Cross-Border Investment: Key Jurisdictions for Japanese Asset Managers and Investors

Guide

Guide

Japanese asset managers and investors often look to the Cayman Islands or Jersey to raise capital internationally or to structure cross-border investment. Each jurisdiction offers its own distinct advantages depending on the target asset class, investment strategy, investor base, regulatory environment and tax considerations.

- The Cayman Islands: The Cayman Islands is the largest offshore domicile globally and the default fund formation jurisdiction for Japanese investors and asset managers. In particular, Cayman unit trusts represent approximately 70% of all foreign investment trust registrations in Japan.

- Jersey: Jersey is a leading and long standing international financial centre with respected expertise in cross border alternative asset investment vehicles, acting as a gateway for overseas capital from Asia into UK and European markets. Jersey fund administrators currently administer over £543.7 billion in assets under management.

Jurisdictional choice can shape everything from speed to market and investor familiarity, to tax neutrality and regulatory alignment.

Below is a comparative guide outlining why Japanese asset managers or investors have chosen the Cayman Islands or Jersey to structure their cross-border investment, with a snapshot comparison table and a series of case studies showcasing typical Cayman Structures or Jersey Structures used by Japanese asset managers or institutional investors to make their cross border investments.

Cayman Islands

Why Japanese asset managers and investors choose the Cayman Islands for funds and investment vehicles

The Cayman Islands is the leading offshore jurisdiction for investment funds and cross border investment vehicles, particularly for private equity, private credit and hedge funds. Its scale and global recognition make it the market standard for international fund launches.

Key strengths

- Tradition and familiarity – The Cayman Islands has been the bridge between Japan and the global funds market since the 1990s. The importance of this relationship is demonstrated by the fact that specific legislative amendments have been made to the Cayman Islands legal regime for the Japanese market.

- Scale: second only to the US – The Cayman Islands has over 30,000 registered funds and more than US$8.5 trillion assets under management.

- Global standard: familiar and credible among investors – Default domicile for private equity and hedge funds outside the US, widely adopted by the largest global fund sponsors. It is highly familiar to institutional investors, banks, and fund administrators worldwide and this familiarity instils confidence and eases operational setup.

- Flexible structuring: the choice for complex strategies – Standalone funds, master-feeders (including Cayman/Delaware combinations) and segregated portfolio companies are all available based on an English common law framework which is internationally accepted. There are no prescribed investment restrictions – no limitation on strategies or asset classes by law.

- No direct taxes: neutral and transparent – No corporate income tax, no capital gains tax, and no withholding taxes on distributions with investors only taxed in their own jurisdictions. The Cayman Islands has also committed to global tax transparency standards (eg FATCA, OECD, CRS), so this neutrality comes with recognized compliance.

- Speed to market: pragmatic and light regulation – Straightforward authorisation and efficient set up compared with onshore jurisdictions.

- Global investor base: reach across regions – Especially popular with US, Asian, Middle Eastern, and Latin American investors, as well as global institutional capital.

Common use cases for the Cayman Islands

- Global private equity funds – The Cayman Islands is the market-leading offshore domicile for global private equity sponsors in the US, Asia and Middle East. It is frequently seen alongside a Luxembourg structure to accommodate EU investors. The Cayman “private equity type” unit trust has become the go-to structure for Japanese investors looking to invest in private markets.

- Hedge funds and liquid trading strategies – The Cayman Islands is the go-to domicile for hedge fund managers, including those running global macro, equity long/short, credit, and multi-strategy funds. Its fund laws are tailored to open-ended funds (the Mutual Funds Act regime), and the master-feeder structures allow parallel Cayman and U.S. vehicles to accommodate different investor types seamlessly.

- Digital asset and crypto funds – Many crypto asset and blockchain-focused funds choose the Cayman Islands for its flexibility and receptive regulatory stance. The jurisdiction’s innovative approach make it suitable for emerging asset classes.

- Hybrid and evergreen structures: The Cayman Islands has opened up the market for Japanese high-net worth and retail investors through investment in hybrid and “evergreen” structures into funds managed by global sponsors. Given the familiarity of Japanese investors with open-ended Cayman fund structures, these semi-liquid structures have been widely adopted to facilitate investment in funds managed by TPG, Blackstone, KKR and many others.

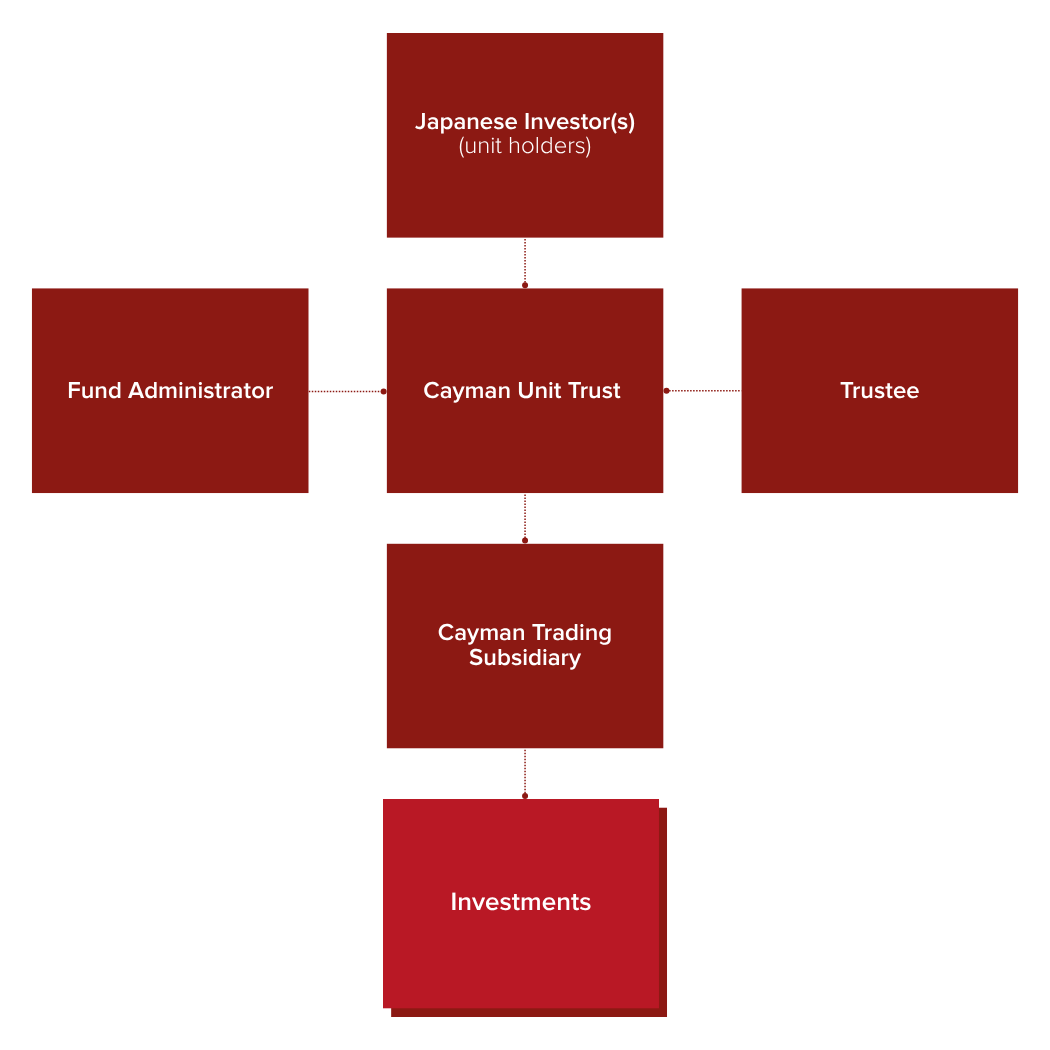

A typical Cayman structure

Private equity type unit trust

Jersey

Why Japanese asset managers choose Jersey for funds and investment vehicles

Jersey has attracted Japanese asset managers and investors through its access to UK and European assets and investors as well as its political and economic stability, its respected regulatory framework and court systems, deep professional service ecosystems, tax neutrality, and global familiarity, particularly to the European and United Kingdom investors and asset management industry.

Key strengths

- Respected regulation tailored to alternative asset classes: global standards with flexibility – Jersey adheres to top-tier global standards (eg, FATF) but with pragmatic regulatory frameworks tailored for the alternative asset management industry. MONEYVAL (the Council of Europe’s permanent monitoring body) has confirmed that Jersey’s effectiveness in preventing financial crime is among the highest worldwide.

- European investor access: efficient and cost effective distribution – Jersey offers straightforward and cost-effective access to UK and European investors via UK or EEA National Private Placement Regimes (NPPRs). Being outside the EEA, Jersey is not subject to the Alternative Investment Fund Managers Directive I or II (AIFMD) when marketing to non EEA investors so has global investor reach.

- Familiarity, Credibility and Speed to Market – Well known and well respected by institutional and sophisticated investors and managers, Jersey is familiar to global fund and asset managers promoting and managing investment into alternative asset classes with a reputation for straightforward and efficient set up and operation of investment vehicles.

- Broad structuring capabilities: solutions for complex arrangements – Jersey is a specialist centre for alternative asset classes. It provides clear, efficient and robust legal and regulatory frameworks for cross border investment into the full range of alternative assets. Options and strategies include public collective investment funds, private funds, co-investments, single asset and single investor vehicles together with carried interest vehicles. This is supported by a wide range of investment vehicle types to match selected investment strategies, including limited partnerships, companies, unit trusts, limited liability companies and cell companies.

- Established ecosystem: global reach and significant professional expertise – Jersey has substantial experience across all types of alternative fund strategies and asset classes with more than 14,000 skilled and experienced finance professionals including lawyers, accountants, trustees, corporate and fund administrators, insurance and technology professionals.

- Tax neutrality and transparency – No income or capital gains taxes and no withholding taxes on distributions or dividends from investment holding structures carrying on international activities from Jersey. This gives operational flexibility with the appropriate tax paid by investors in their own jurisdictions and/or in the jurisdictions in which the assets are located. Jersey’s tax neutrality is combined with adherence to global tax transparency standards (OECD, FATCA, CRS).

Common use cases for Jersey for Japanese managers

- Jersey Private Funds – A private funds regime designed for professional and sophisticated investors. Key features include:

| Feature | Shared Characteristics |

| Fast-track Authorisation | Regulatory approvals in as little as 1 business day via a streamlined process |

| Investors | No restriction on the number of investors. Investors must be professional, eligible or sophisticated investors or invest a minimum amount (£250,000) |

| European Marketing | European marketing is possible in specified jurisdictions under the local National Private Placement Rules in the EEA or the United Kingdom |

| Audit | Local audit optional |

- Cross-border investment by global and institutional asset managers and investors into alternative asset classes – Private equity, venture capital, real estate, private credit, infrastructure and niche alternative strategies.

- Global private equity funds – Sophisticated and institutional investors access private equity strategies through Jersey funds promoted by global sponsors, often alongside a Luxembourg sleeve for EU investors.

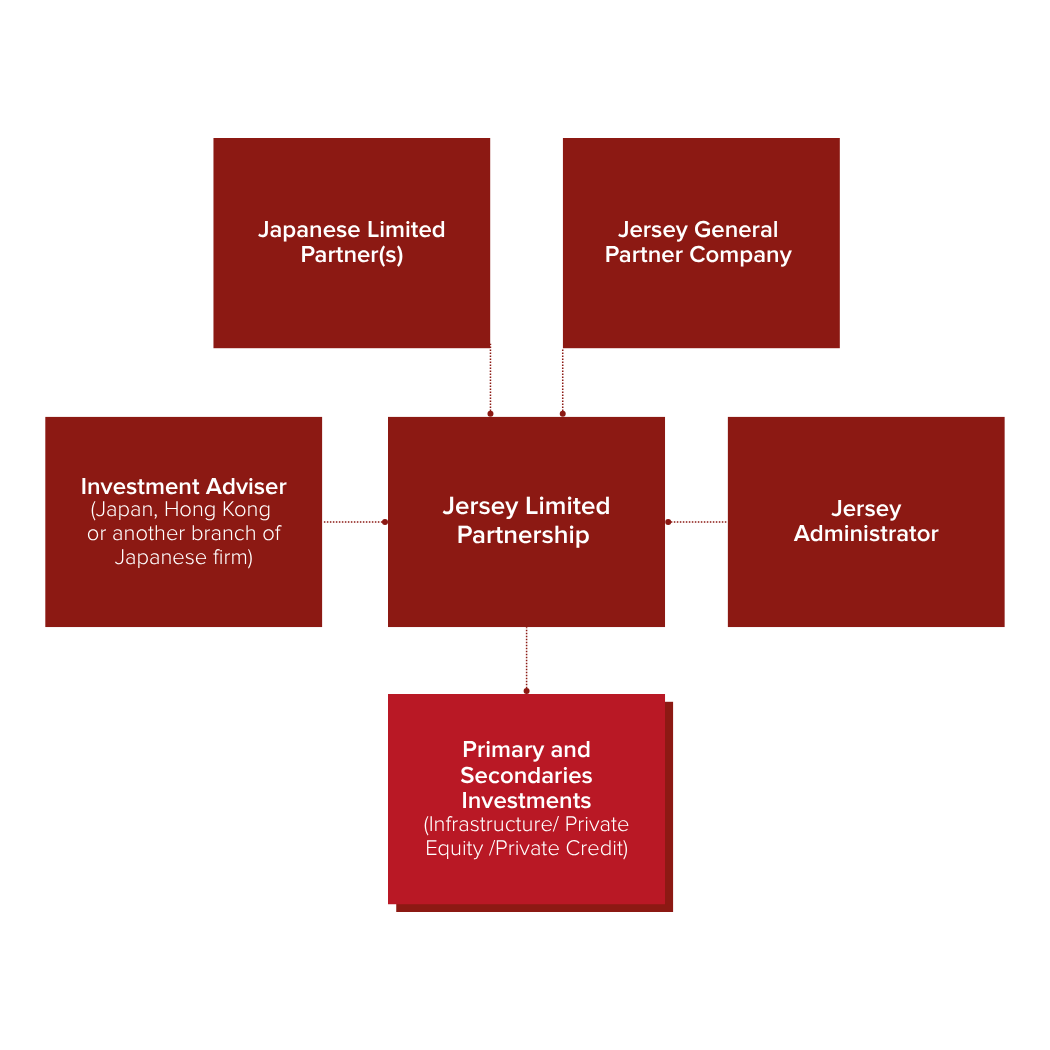

Jersey use cases for Japanese asset managers and institutional investors

Fund of Funds with a private equity/infrastructure/private credit focus

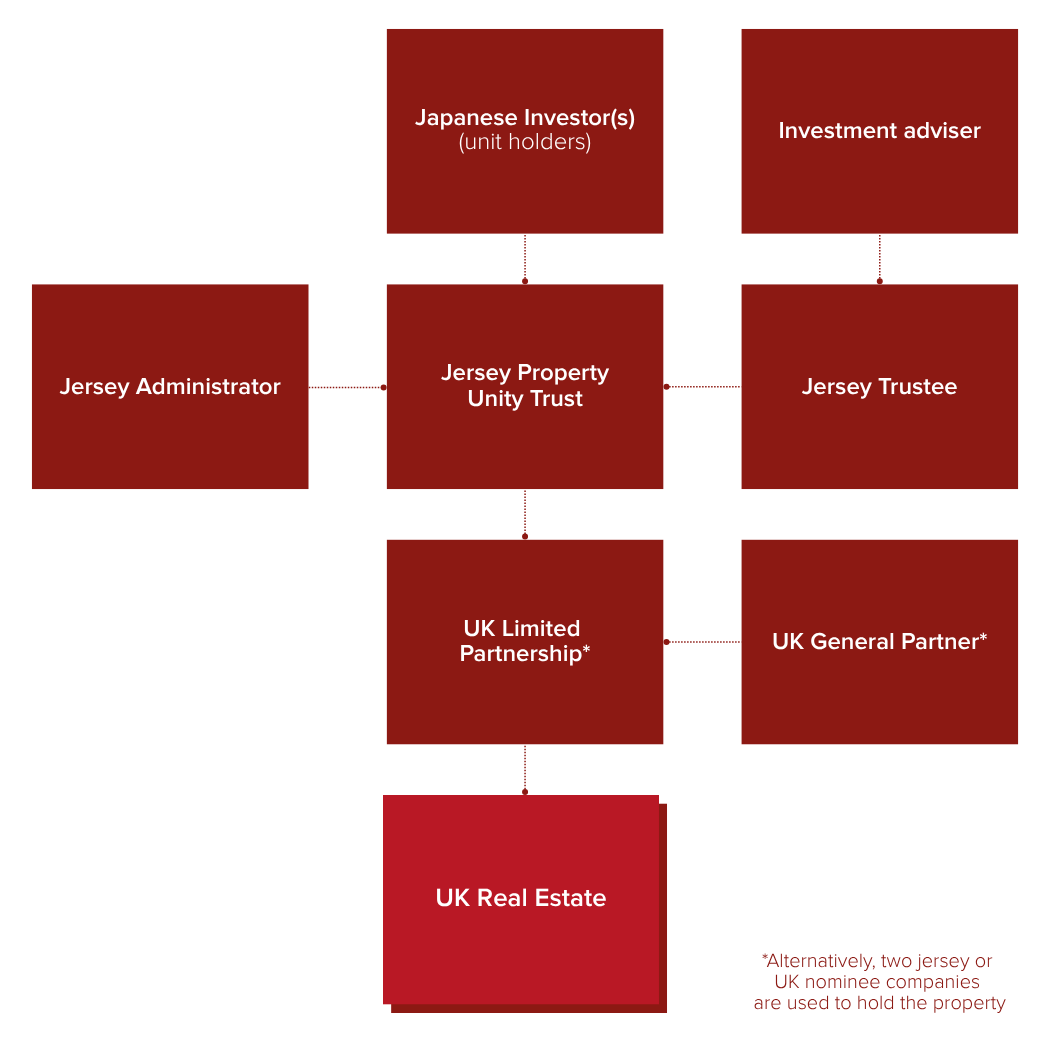

UK real estate investment – Jersey is a common choice for direct and indirect investment into UK real estate assets and is very familiar to UK real estate investors and asset management professionals.

The most common Jersey investment vehicles is either a Jersey limited partnership for most private capital strategies or a Jersey property unit trust for investment into UK real estate.

Jersey property unit trust for investment into UK real estate

Jurisdiction comparison snapshot

To help illustrate the differences at a glance, the table below compares key features of the Cayman Islands, and Jersey for vehicles for cross border investment:

| Feature | Cayman Islands | Jersey |

| EU Market Access | Via NPPR (private placement in UK and specific EEA countries) where allowed for registered or non-EU AIFMs | Via NPPR (private placement in UK and specific EEA countries) where allowed for registered or non-EU AIFMs |

| Regulation | Light – pragmatic regulation | Light – robust oversight but flexible |

| Tax Regime | Tax-neutral (no corporate, income or capital gains taxes) | Tax-neutral (no corporate, income or capital gains taxes) |

| Setup Speed | Fast – can launch quickly | Fast – approvals in as little as one day for Jersey Private Funds |

| Common Users | Large cap private equity and hedge funds for institutional fund sponsors targeting US, Asia and Middle East investors in particular. | Private equity, venture capital, real estate managers (esp. Europe-focused); mid-sized alternative managers, club deal organisers |

How Mourant can help

With specialist teams across all four jurisdictions, together with on-the-ground expertise in our key city locations of Hong Kong, Singapore, and London, we are well positioned to provide seamless support across multiple time zones.

Mourant is ideally placed to assist Japanese asset managers and investors across the full lifecycle of a fund, from structuring and establishment through to ongoing administration. We bring together experienced lawyers and professional services teams in Cayman and Jersey, including our integrated fund administration offering, and work closely with Japanese counsel and service providers to ensure smooth implementation and ongoing cross-border compliance.

Whether launching a new strategy, accessing global capital, or navigating complex cross-border investments, our cross-jurisdictional expertise and commercial insight can help structure for success. We advise on the nuances of each domicile, from fast-tracking a Jersey Private Fund to establishing a Cayman master-feeder structure, always tailoring solutions to your investor base and commercial objectives.

Our goal is to make the fund lifecycle, from formation through to ongoing administration as efficient and seamless as possible, while ensuring it remains fully aligned with your strategic needs.

Contacts

A full list of contacts can be found here.

Contact

Alex Last

Felicia de Laat

This guide is only intended to give a summary and general overview of the subject matter. It is not intended to be comprehensive and does not constitute, and should not be taken to be, legal advice. If you would like legal advice or further information on any issue raised by this guide, please get in touch with one of your usual contacts. You can find out more about us, and access our legal and regulatory notices at mourant.com. © 2026 MOURANT ALL RIGHTS RESERVED

Investment Funds

Guide

Guide

3 August 2026

Guernsey’s economic substance requirements

Update

Guide

28 July 2026

Mergers – a comparison

Guide

Guide

Guide

Guide

28 July 2026

Offshore Corporate Structures – a comparison

Guide

Guide

Sign up

Subscribe to keep up-to-date with the latest news, updates, legal guides and thought leadership articles.

Ready to take the next step? Let’s talk.

Send our team a message and we’ll be back in touch with you.