Schemes of Arrangement under Jersey Law

Guide

Guide

What is a scheme of arrangement?

A scheme of arrangement (a Scheme) is a court-sanctioned compromise or arrangement between a company and its creditors or members (or any class of them) in accordance with Part 18A of the Companies (Jersey) Law 1991 (the Law), specifically sections 125 to 127 (inclusive). The Jersey provisions on Schemes are largely similar to those in England, save that the ‘headcount’ test no longer applies in Jersey as discussed below.

Whilst the scope for using a Scheme is wide, this guide only considers Schemes between a company and its members in the context of a takeover bid.

Statutory requirements

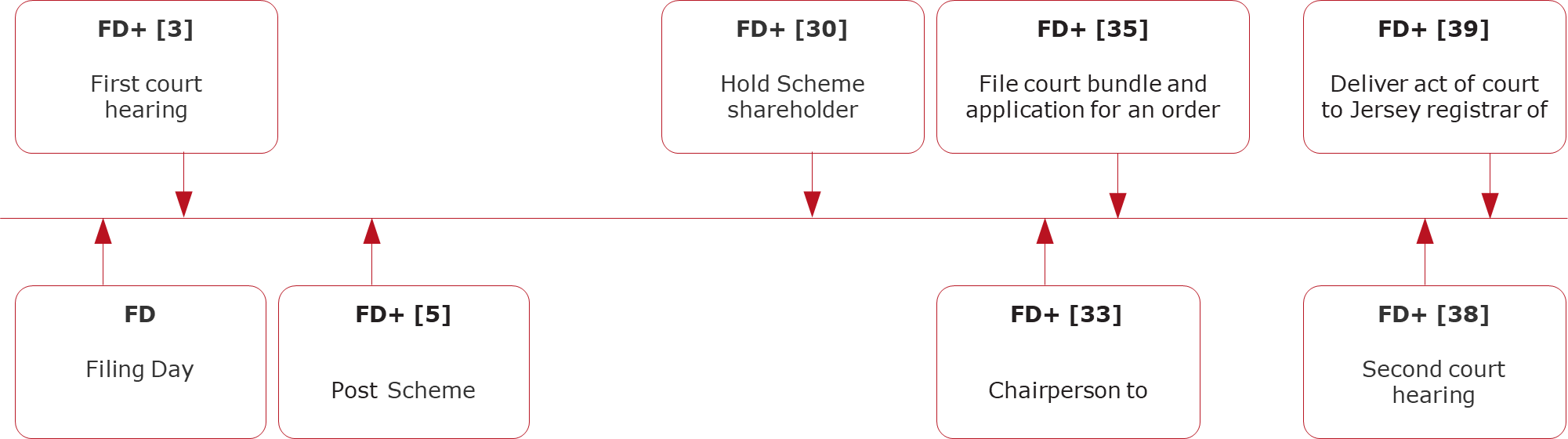

Following an application by the company, or any of its members, the court will hold a hearing to consider whether to order a meeting of the company’s members (or the relevant classes concerned) to vote on the proposed Scheme (the Directions Hearing).

To proceed, the Scheme must be approved at the court-ordered meeting(s) by members (or the relevant classes of members) holding at least 75 per cent of the voting rights of those present and voting, whether in person or by proxy. The requirement to obtain the approval of a majority in number of members (often referred to as the ‘headcount test’) was removed following the coming into force of the Companies (Jersey) Amendment Law 2026 on 1 June 2026.

After the Scheme has been approved by the requisite majority of members, it must then be sanctioned by the court at the second court hearing (the Sanction Hearing). The Scheme becomes effective when the relevant act of court is delivered to the Jersey registrar of companies for registration. Once effective, the Scheme is binding on all members (or all members of the relevant class) and, where the company is being wound up, on the liquidator and contributories of the company or, in the case of a company in administration, on the administrator and the company’s contributories.

Because the Jersey provisions on Schemes are largely similar to those in England, the courts in Jersey, although not bound by the decisions of the English courts, have tended to find these persuasive when dealing with both the procedural and substantive issues associated with Schemes.

Why use a Scheme?

The biggest advantage of a Scheme (over other takeover alternatives) is the certainty around acquiring 100 per cent of the target company. If the court has sanctioned a Scheme, all the members of the class concerned are bound whether they voted in favour of the Scheme or not.

Although under a traditional takeover offer (as opposed to a Scheme) only a holding of shares carrying over 50 per cent of the voting rights is required to obtain control, in order to acquire 100 per cent of the target, the bidder needs acceptances into the bid of not less than 90 per cent in value or number of the shares to which the offer relates in order for the bidder to exercise its statutory squeeze out rights for the remaining outstanding shares. This is in contrast to a Scheme where, subject to receiving a vote in favour of the proposal by 75 per cent of the voting rights of the members present and voting in person or by proxy, all members of that class will be forced into the bid.

Another potential advantage of using a Scheme over a traditional takeover bid is that the period for acquiring 100 per cent control can, in circumstances, be shorter under a Scheme than a takeover offer because of the time limits imposed by the statutory squeeze-out procedures.

The Law also permits two Jersey companies to merge, or a Jersey company to merge with a non-Jersey company. The merger provisions of the Law can also be used to give effect to a takeover of a Jersey company. The shareholder approval threshold for a merger is a special resolution of the members (which, unless the articles of association of that company state otherwise, requires two-thirds or more of the voting rights of the members voting on that resolution). Under the Law, members and creditors have a right to object to a merger.

Though flexible, a Scheme is not suitable for every eventuality. Although there are comparatively few,

the disadvantages are worth being conscious of when considering if your strategic aim is best met by deploying a Scheme, or some other takeover method. Disadvantages include, among other things:

- the inability of a bidder to control the process such that the target and its directors control the timetable and ultimately the implementation of the Scheme;

- the consideration of differing class rights in that there may be a requirement for different Scheme meetings to account for different classes; and

- procedural complexities that stem from involving the courts in the takeover process.

The Scheme procedure

There are four main steps involved in undertaking a Scheme which broadly mirror the process in the UK. These are: application to the court at the Directions Hearing for an order to call a Scheme meeting of members; Scheme meeting notification (including the despatch of Scheme documentation); the Scheme meeting itself; and the application to the court at the Sanction Hearing for sanction of the Scheme. Expanded, these are as follows:

- The company will file an application with the court for an order requisitioning a meeting of members (or class of members, as the case may be) to consider and vote on the proposed Scheme. The application will also request for any directions to be given by the court. This is the Directions Hearing. The company will be represented at the hearing by a Jersey advocate, which would typically be a partner in our litigation team.

- Every notice summoning the court meeting(s) that is sent to members must be accompanied by a statement complying with the Law. The disclosure requirements are comprised in the Scheme circular to members and, among other things, include information on: the effects of implementation of the Scheme; the consideration payable (being cash, shares or a combination of both); the disclosure of any material interests of the directors (whether in their capacity as directors or otherwise) and the effect on those interests of the compromise or arrangement, in so far as it is different from the effect on the like interests of other persons; and generally must, as far as possible, give all information reasonably necessary to enable the members to decide how to vote at the meeting.

- At the convened court meeting, the Scheme must be approved by members (or the relevant class of members) holding at least 75 per cent of the voting rights of those present and voting, whether in person or by proxy. Usually, immediately following the court meeting, a general meeting of the company is held to approve certain amendments to the company’s articles of association to help facilitate the Scheme.

- A second court application is then made to the court for it to sanction the Scheme. This is the Sanction Hearing. The court has stated that in exercising its discretion, it will follow the settled approach of the English courts. It is therefore necessary to consider whether:

- the statutory requirements set out in the Law have been complied with;

- each relevant class of member was fairly represented by those who attended the meeting(s) ordered by the court the statutory majority are acting in good faith and are not coercing the minority in order to promote interests adverse to those whom they purport to represent;

- the Scheme is such that an intelligent and honest person, a member of the class concerned and acting in respect of their interest, might reasonably approve; and

- viewing matters in the round, there was a blot on the scheme which might indicate that the court’s discretion should not be exercised in favour of sanctioning the Scheme.

Timing to implement a Scheme

The court timetable for a scheme is established upfront. Overall time from the commencement of proceedings (i.e. the Directions Hearing) to implementation of the Scheme (i.e. the Scheme becoming effective) will be a minimum of four to six weeks, but factors such as court availability and conditionality to the Scheme (for example any requirement for regulatory and/or competition clearances) can extend the timetable.

UK Takeovers Code and JFSC regulated/TISE listed companies

When a Scheme or other proposal is designed to affect a takeover, subject to the status of the target, the Takeover Panel (the Panel) and the City Code on Takeovers and Mergers (the Code) may have a role to play. The Panel’s role will mainly be concerned to ensure the documentation complies with the Code, but consideration needs to be given to these regulations prior to launching a Scheme.

In addition to the standard court process, companies regulated by the Jersey Financial Services Commission (the JFSC) or listed on The International Stock Exchange (TISE) will need to liaise with the JFSC or TISE (as the case may be) regarding the Scheme in accordance with applicable rules.

Contacts

A list of contacts specialising in corporate law can be found here.

Contact

James Hill

Andrew Salisbury

This guide is only intended to give a summary and general overview of the subject matter. It is not intended to be comprehensive and does not constitute, and should not be taken to be, legal advice. If you would like legal advice or further information on any issue raised by this guide, please get in touch with one of your usual contacts. You can find out more about us, and access our legal and regulatory notices at mourant.com. © 2026 MOURANT ALL RIGHTS RESERVED

Corporate and M&A

Update

Update

6 July 2026

Caribbean Regulatory Update – Q3 2026

News

News

Update

Update

News

News

Guide

Guide

23 June 2026

A guide to the Security Interests (Jersey) Law 2012

Guide

Guide

23 June 2026

The Company Secretary’s Survival Guide

Sign up

Subscribe to keep up-to-date with the latest news, updates, legal guides and thought leadership articles.

Ready to take the next step? Let’s talk.

Send our team a message and we’ll be back in touch with you.